Blogs

Why does New York state sue its college students? Thousands have been taken to court, and can defend themselves only in Albany — even if they live hundreds of miles away?

This article can be found at Hechinger Report at https://hechingerreport.org/new-york-states-attorney-general-sues-suny-s...

Clark Howard shares some advice on how to improve credit scores.

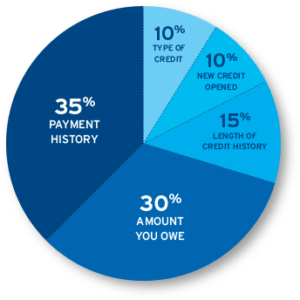

In order to improve your credit score, it is important to understand the factors that go into calculating your score. The chart below shows the 5 factors that go into improving credit. It also shows how much each factor matters when it comes to improving credit scores.

Payment History– This factor is the most important factor. “Not paying your bills on time can do serious damage to your credit score. Even if you’ve had some late payments in the past, you can improve your score going forward by paying each and every bill on time. Not paying your bills on time can do serious damage to your credit score. Even if you’ve had some late payments in the past, you can improve your score going forward by paying each and every bill on time.”

Payment History– This factor is the most important factor. “Not paying your bills on time can do serious damage to your credit score. Even if you’ve had some late payments in the past, you can improve your score going forward by paying each and every bill on time. Not paying your bills on time can do serious damage to your credit score. Even if you’ve had some late payments in the past, you can improve your score going forward by paying each and every bill on time.”

Amounts Owed– This is the second most important factor. This factor is calculated as a percentage. “The amount you owe divided by the total amount of credit you have available. It’s best to keep this under 30% — even better if you can keep it under 10%. So if your total credit line (between all of your credit cards and other loans) is $10,000, it’s good to owe less than $3,000 and great if you owe less than $1,000.”

Length of Credit History– The next most important factor is how long you’ve had credit. “This is determined by the date you opened your oldest credit account that’s still active. Since you can’t go back in time and open an account any earlier, the most important thing you can do in this area is to make sure you don’t close any of your old accounts.”

New Credit & Credit Mix– New credit & the type of credit amount for 10% each. New credit is credit that you’ve recently applied for. Any time you apply for credit, your score will drop. It won’t take long to recover. Just remember to only apply for credit you really need. “Your credit mix refers to the different types of credit you have.” Someone with just credit cards will be less favorable than someone with credit cards, a mortgage, and a car loan.

Bankruptcy is also a fast way you can fix your score! How? Click here to find out more!

.fusion-button.button-1 {border-radius:2px;}Read The Full Article.fusion-body .fusion-builder-column-0{width:100% !important;margin-top : 0px;margin-bottom : 0px;}.fusion-builder-column-0 > .fusion-column-wrapper {padding-top : 0px !important;padding-right : 0px !important;margin-right : 1.92%;padding-bottom : 0px !important;padding-left : 0px !important;margin-left : 1.92%;}@media only screen and (max-width:1138px) {.fusion-body .fusion-builder-column-0{width:100% !important;}.fusion-builder-column-0 > .fusion-column-wrapper {margin-right : 1.92%;margin-left : 1.92%;}}@media only screen and (max-width:900px) {.fusion-body .fusion-builder-column-0{width:100% !important;}.fusion-builder-column-0 > .fusion-column-wrapper {margin-right : 1.92%;margin-left : 1.92%;}}.fusion-body .fusion-flex-container.fusion-builder-row-1{ padding-top : 0px;margin-top : 0px;padding-right : 0px;padding-bottom : 0px;margin-bottom : 0px;padding-left : 0px;}

The post How You Can Improve Your Credit Score! appeared first on Allmand Law Firm, PLLC.

Clark Howard shares some advice on how to improve credit scores.

In order to improve your credit score, it is important to understand the factors that go into calculating your score. The chart below shows the 5 factors that go into improving credit. It also shows how much each factor matters when it comes to improving credit scores.

Payment History– This factor is the most important factor. “Not paying your bills on time can do serious damage to your credit score. Even if you’ve had some late payments in the past, you can improve your score going forward by paying each and every bill on time. Not paying your bills on time can do serious damage to your credit score. Even if you’ve had some late payments in the past, you can improve your score going forward by paying each and every bill on time.”

Amounts Owed– This is the second most important factor. This factor is calculated as a percentage. “The amount you owe divided by the total amount of credit you have available. It’s best to keep this under 30% — even better if you can keep it under 10%. So if your total credit line (between all of your credit cards and other loans) is $10,000, it’s good to owe less than $3,000 and great if you owe less than $1,000.”

Length of Credit History– The next most important factor is how long you’ve had credit. “This is determined by the date you opened your oldest credit account that’s still active. Since you can’t go back in time and open an account any earlier, the most important thing you can do in this area is to make sure you don’t close any of your old accounts.”

New Credit & Credit Mix– New credit & the type of credit amount for 10% each. New credit is credit that you’ve recently applied for. Any time you apply for credit, your score will drop. It won’t take long to recover. Just remember to only apply for credit you really need. “Your credit mix refers to the different types of credit you have.” Someone with just credit cards will be less favorable than someone with credit cards, a mortgage, and a car loan.

Bankruptcy is also a fast way you can fix your score! How? Click here to find out more!

.fusion-button.button-9 {border-radius:2px;}Read The Full Article.fusion-body .fusion-builder-column-8{width:100% !important;margin-top : 0px;margin-bottom : 0px;}.fusion-builder-column-8 > .fusion-column-wrapper {padding-top : 0px !important;padding-right : 0px !important;margin-right : 1.92%;padding-bottom : 0px !important;padding-left : 0px !important;margin-left : 1.92%;}@media only screen and (max-width:1138px) {.fusion-body .fusion-builder-column-8{width:100% !important;}.fusion-builder-column-8 > .fusion-column-wrapper {margin-right : 1.92%;margin-left : 1.92%;}}@media only screen and (max-width:900px) {.fusion-body .fusion-builder-column-8{width:100% !important;}.fusion-builder-column-8 > .fusion-column-wrapper {margin-right : 1.92%;margin-left : 1.92%;}}.fusion-body .fusion-flex-container.fusion-builder-row-9{ padding-top : 0px;margin-top : 0px;padding-right : 0px;padding-bottom : 0px;margin-bottom : 0px;padding-left : 0px;}

The post How You Can Improve Your Credit Score! appeared first on Allmand Law Firm, PLLC.

Debt relief, debt adjusting, or debt settlement services are often offered by companies that claim that they can negotiate with your creditors to reduce the amount you owe. Aside from the fact that there are many caveats, it is essential to remember that debt forgiveness may come with certain tax consequences. If the creditor forgives a portion of your debt, it could be counted as taxable income on your federal income taxes.

It is best to seek legal advice before agreeing to work with any debt settlement company with these things in mind. Consider all of your options, including negotiating directly with the debt collector or creditor or filing for bankruptcy instead. A trusted Oregon bankruptcy attorney can explain the pros and cons of your legal options and explain how a forgiven debt can affect your federal income tax.

Debt Relief Solutions

Debt relief solutions are often advertised by companies who claim that they can settle, renegotiate, or in some way change the terms of debt with a creditor or debt collector. Dealing with debt settlement companies is often confused with debt consolidation, but the two have significant differences and risk levels.

The term ‘debt consolidation’ refers to a process of taking out a loan at a relatively low interest rate and using the borrowed funds to pay off debts with high-interest rates. Considering its original meaning, consolidating debts enables a debtor to replace multiple monthly bills with one predictable monthly payment. This can save you money by reducing the interest you pay over time and simplifying your bill-paying and budgeting routines.

Debt consolidation is often preferred over the services offered by debt relief companies. They often make payments to creditors on your behalf through the single monthly payment made to them.

Things to Consider When Looking Into Debt Relief Solutions

It is crucial to exercise due diligence before dealing with debt relief companies that promise unrealistically huge savings by renegotiating debt with creditors. Your credit report is subject to considerable risk in some cases, but you could still face financially unfavorable circumstances. You may consider many options to get your debts under control, but for some people, debt relief services are not advisable.

In general, credit scores are significantly affected when entries in your credit report are new. Most of the time, before debtors consider debt relief, their credit reports have already been negatively affected by late or missed payments. The severity of their impact will depend on the nature and number of negative entries and how high your score was before you began struggling with debt repayment. While your credit score will gradually improve, some of the entries will stay for several years.

Alternatives to Debt Relief Services

While some people are indeed able to reach their goals through debt relief companies, there are other ways of dealing with your secured and unsecured debts.

There is a small number of debt management programs offered by non-profit debt management organizations. Some volunteer credit counselors can help you organize your budget and take control of your debts.

Others may even work with your creditors to develop extended repayment schedules or interest rate reductions that can help you pay your debts in full. These, however, would involve paying off what you owe, and these organizations may be loaded with cases.

Meanwhile, having a balance transfer credit card is a somewhat less risky version of debt consolidation. This involves moving debt from one or more high-interest credit card accounts to a lower interest card account, particularly one with a 0% introductory annual percentage rate (APR) on balance transfers. The catch, however, is that such a card would require good credit, which you might no longer have. Additionally, failure to pay off your balance transfer within the introductory period could lead to unwanted fees and interest charges.

Filing Bankruptcy

In many cases, the best option to deal with overwhelming unsecured and secured debts is to file for bankruptcy. Due to automatic stay, it is a reasonably quick way to get rid of the stress brought about by constant calls and letters from debt collectors. Additionally, while a Chapter 7 bankruptcy petition can remain on your credit report for several years, its negative effect lessens over time. The eventual rebuilding of your credit and borrowing power can be difficult but not impossible.

Seek Legal Help from Hands-on Oregon Bankruptcy Lawyers

Debt settlement can get expensive due to the fees that debt relief companies charge. Additionally, if a settlement company succeeds in having your debt forgiven. In that case, your debt may be treated as income for purposes when calculating your federal income tax. You could end up paying at least a portion of a forgiven debt to the IRS, depending on your earnings, deductions, and tax bracket.

If your income and other financial circumstances make it almost impossible for you to pay even renegotiated debts, filing for bankruptcy may be your only choice. Here, a reliable Portland bankruptcy law firm can help. Consult with a dedicated Oregon bankruptcy lawyer at Northwest Debt Relief Law Firm today.

The post How Do Debt Relief Services Work? appeared first on Portland Bankruptcy Attorney | Northwest Debt Relief Law Firm.

“Diane is an excellent Bankruptcy Attorney – five stars ” M.W.

“Diane is an excellent Bankruptcy Attorney – five stars ” M.W.

Five stars. Diane is an excellent Bankruptcy Attorney. She guided my wife and I through the entire process.

Five stars. Diane is an excellent Bankruptcy Attorney. She guided my wife and I through the entire process.

We highly recommend her to anyone who needs to file a bankruptcy. M.W.

.fusion-body .fusion-builder-column-0{width:100% !important;margin-top : 0px;margin-bottom : 20px;}.fusion-builder-column-0 > .fusion-column-wrapper {padding-top : 0px !important;padding-right : 0px !important;margin-right : 1.92%;padding-bottom : 0px !important;padding-left : 0px !important;margin-left : 1.92%;}@media only screen and (max-width:980px) {.fusion-body .fusion-builder-column-0{width:100% !important;order : 0;}.fusion-builder-column-0 > .fusion-column-wrapper {margin-right : 1.92%;margin-left : 1.92%;}}@media only screen and (max-width:640px) {.fusion-body .fusion-builder-column-0{width:100% !important;order : 0;}.fusion-builder-column-0 > .fusion-column-wrapper {margin-right : 1.92%;margin-left : 1.92%;}}.fusion-body .fusion-flex-container.fusion-builder-row-1{ padding-top : 0px;margin-top : 0px;padding-right : 0px;padding-bottom : 0px;margin-bottom : 0px;padding-left : 0px;}

The post She guided us through the entire process – five stars appeared first on Diane L. Drain - Phoenix Arizona Bankruptcy Attorney.

“You can feel confident in her ability to provide you with any and all answers that may arise. ” D.L.

I can’t say enough about the professionalism for Diane Drain and Jay. She helped me maneuver the process of Bankruptcy through an unusual situation. I highly recommend Diane Drain. You can feel confident in her ability to provide you with any and all answers that may arise. Don’t hesitate to call her. D.L.

.fusion-body .fusion-builder-column-0{width:100% !important;margin-top : 0px;margin-bottom : 20px;}.fusion-builder-column-0 > .fusion-column-wrapper {padding-top : 0px !important;padding-right : 0px !important;margin-right : 1.92%;padding-bottom : 0px !important;padding-left : 0px !important;margin-left : 1.92%;}@media only screen and (max-width:980px) {.fusion-body .fusion-builder-column-0{width:100% !important;order : 0;}.fusion-builder-column-0 > .fusion-column-wrapper {margin-right : 1.92%;margin-left : 1.92%;}}@media only screen and (max-width:640px) {.fusion-body .fusion-builder-column-0{width:100% !important;order : 0;}.fusion-builder-column-0 > .fusion-column-wrapper {margin-right : 1.92%;margin-left : 1.92%;}}.fusion-body .fusion-flex-container.fusion-builder-row-1{ padding-top : 0px;margin-top : 0px;padding-right : 0px;padding-bottom : 0px;margin-bottom : 0px;padding-left : 0px;}

The post Diane Helped me Maneuver the Process of Bankruptcy Through an Unusual Situation appeared first on Diane L. Drain - Phoenix Arizona Bankruptcy Attorney.

“We highly recommend Diane Drain IF you are looking for the educated, knowledgeable, honest and transparent (and very fairly priced) attorney! ” P.R.

“We had recently relocated to Arizona from the Chicago area when we realized we had to face up to our financial problems, rather than run away from them. Our Chicago attorney was helpful in assisting us in choosing the right bankruptcy attorney – boy did he pick the perfect person!! Diane talked us through every step of the process! Our emotional ups and downs were frequent, and her patience was unwavering! We highly recommend Diane Drain IF you are looking for the educated, knowledgeable, honest and transparent (and very fairly priced) attorney! If you want a flash in the pan, “Bankruptcy for $199″ and get it done in 72 hours” good luck to you! Diane has earned high praises from our other attorney, our accountant and our Chicago attorney, who has her on his referral list for clients moving to Arizona.

“We had recently relocated to Arizona from the Chicago area when we realized we had to face up to our financial problems, rather than run away from them. Our Chicago attorney was helpful in assisting us in choosing the right bankruptcy attorney – boy did he pick the perfect person!! Diane talked us through every step of the process! Our emotional ups and downs were frequent, and her patience was unwavering! We highly recommend Diane Drain IF you are looking for the educated, knowledgeable, honest and transparent (and very fairly priced) attorney! If you want a flash in the pan, “Bankruptcy for $199″ and get it done in 72 hours” good luck to you! Diane has earned high praises from our other attorney, our accountant and our Chicago attorney, who has her on his referral list for clients moving to Arizona.

Bankruptcy is a big deal and not something to put in the hands of anyone less than the best!” P.R.

.fusion-body .fusion-builder-column-0{width:100% !important;margin-top : 0px;margin-bottom : 20px;}.fusion-builder-column-0 > .fusion-column-wrapper {padding-top : 0px !important;padding-right : 0px !important;margin-right : 1.92%;padding-bottom : 0px !important;padding-left : 0px !important;margin-left : 1.92%;}@media only screen and (max-width:980px) {.fusion-body .fusion-builder-column-0{width:100% !important;order : 0;}.fusion-builder-column-0 > .fusion-column-wrapper {margin-right : 1.92%;margin-left : 1.92%;}}@media only screen and (max-width:640px) {.fusion-body .fusion-builder-column-0{width:100% !important;order : 0;}.fusion-builder-column-0 > .fusion-column-wrapper {margin-right : 1.92%;margin-left : 1.92%;}}.fusion-body .fusion-flex-container.fusion-builder-row-1{ padding-top : 0px;margin-top : 0px;padding-right : 0px;padding-bottom : 0px;margin-bottom : 0px;padding-left : 0px;}

The post Our Emotional Ups and Downs Were Frequent, and Her Patience Was Unwavering! appeared first on Diane L. Drain - Phoenix Arizona Bankruptcy Attorney.

The New York Post reveals that lawyers have collected a mere $1.4 million for the attendees of Fyre Festival after 4 years of trying to collect funds. After subtracting the funds for the legal team, attendees are to split $300,000. This will leave about 4 cents on the dollar for the ticket holders. Ticket holders claim they are owed $7 million.

In The Know: Fyre Festival was a failed music festival created by entrepreneur Billy McFarland and rapper Ja Rule. Fyre Festival was advertised as a luxury music festival in the Bahamas. Celebrities such as Kendall Jenner and Emily Ratajkowski promoted the festival. Bands such as Blink-182 and Major Lazer were scheduled to perform. Festival attendees spent $1,200 minimum on tickets with additional packages costing up to $100,000. Attendees arrived at the festival expecting luxury accommodations and food. Instead, they found cold cheese sandwiches and FEMA tents to sleep in. All musical acts bailed & the models failed to disclose that they were paid to promote the festival. Attendees were left confused and with no real place to stay.

McFarland is now serving a six-year jail sentence for fraud.

Fyre Festival’s bankruptcy trustee Gregory Messner claims over the last four years he has tried to collect money from the models & bands who benefited from this scheme. Messner claims Kendall Jenner coughed up less than half of the money she was paid for promoting the event. Emily Ratajkowski gave back a measly 10% of the money she earned and Blink-182 gave back more than half of the money. McFarland did nothing to help recover funds and barely kept any books and records that could help track down any additional person who benefited from this disastrous scheme.

Messner is looking into whether documentary footage from Netflix and Hulu is estate property. Otherwise, he aims to earn the court’s approval to close the case as soon as possible.

From the Article:

“Bankruptcy expert Adam Stein-Sapir thinks the burned Fyre Festival creditors who stand to get paid should count themselves lucky, despite the pitiful recovery. ‘The reality is that there were almost no business records to speak of, no paper trail showing exactly how money came in and where it went, so the fact that there was anything left over is a bit of a win,’ Stein-Sapir said.”

.fusion-button.button-1 {border-radius:2px;}Read The Full Article.fusion-body .fusion-builder-column-0{width:100% !important;margin-top : 0px;margin-bottom : 0px;}.fusion-builder-column-0 > .fusion-column-wrapper {padding-top : 0px !important;padding-right : 0px !important;margin-right : 1.92%;padding-bottom : 0px !important;padding-left : 0px !important;margin-left : 1.92%;}@media only screen and (max-width:1138px) {.fusion-body .fusion-builder-column-0{width:100% !important;}.fusion-builder-column-0 > .fusion-column-wrapper {margin-right : 1.92%;margin-left : 1.92%;}}@media only screen and (max-width:900px) {.fusion-body .fusion-builder-column-0{width:100% !important;}.fusion-builder-column-0 > .fusion-column-wrapper {margin-right : 1.92%;margin-left : 1.92%;}}.fusion-body .fusion-flex-container.fusion-builder-row-1{ padding-top : 0px;margin-top : 0px;padding-right : 0px;padding-bottom : 0px;margin-bottom : 0px;padding-left : 0px;}

The post Fyre Festival Attendees To Recover Nothing From Bankruptcy appeared first on Allmand Law Firm, PLLC.

“We highly recommend Diane Drain IF you are looking for the educated, knowledgeable, honest and transparent (and very fairly priced) attorney! ” P.R.

We had recently relocated to Arizona from the Chicago area when we realized we had to face up to our financial problems, rather than run away from them. Our Chicago attorney was helpful in assisting us in choosing the right bankruptcy attorney – boy did he pick the perfect person!! Diane talked us through every step of the process! Our emotional ups and downs were frequent, and her patience was unwavering! We highly recommend Diane Drain IF you are looking for the educated, knowledgeable, honest and transparent (and very fairly priced) attorney! If you want a flash in the pan, “Bankruptcy for $199″ and get it done in 72 hours” good luck to you! Diane has earned high praises from our other attorney, our accountant and our Chicago attorney, who has her on his referral list for clients moving to Arizona.

Bankruptcy is a big deal and not something to put in the hands of anyone less than the best!” P.R.

.fusion-body .fusion-builder-column-1{width:100% !important;margin-top : 0px;margin-bottom : 20px;}.fusion-builder-column-1 > .fusion-column-wrapper {padding-top : 0px !important;padding-right : 0px !important;margin-right : 1.92%;padding-bottom : 0px !important;padding-left : 0px !important;margin-left : 1.92%;}@media only screen and (max-width:980px) {.fusion-body .fusion-builder-column-1{width:100% !important;order : 0;}.fusion-builder-column-1 > .fusion-column-wrapper {margin-right : 1.92%;margin-left : 1.92%;}}@media only screen and (max-width:640px) {.fusion-body .fusion-builder-column-1{width:100% !important;order : 0;}.fusion-builder-column-1 > .fusion-column-wrapper {margin-right : 1.92%;margin-left : 1.92%;}}.fusion-body .fusion-flex-container.fusion-builder-row-2{ padding-top : 0px;margin-top : 0px;padding-right : 0px;padding-bottom : 0px;margin-bottom : 0px;padding-left : 0px;}

The post Our Emotional Ups and Downs Were Frequent, and Her Patience Was Unwavering! appeared first on Diane L. Drain - Phoenix Arizona Bankruptcy Attorney.

People thinking about filing for bankruptcy will usually do some research before contacting our experienced Roseville bankruptcy lawyers. One of the first things they will discover is that there are different types of types, or chapters, of bankruptcy filings. This begs the question, “which type is the most beneficial for me?” If you are an […]

The post How Do I Know Which Type of Bankruptcy is Best For Me? appeared first on The Bankruptcy Group, P.C..

Learn more about how Bankruptcy works and what you need to know.

Learn more about how Bankruptcy works and what you need to know.